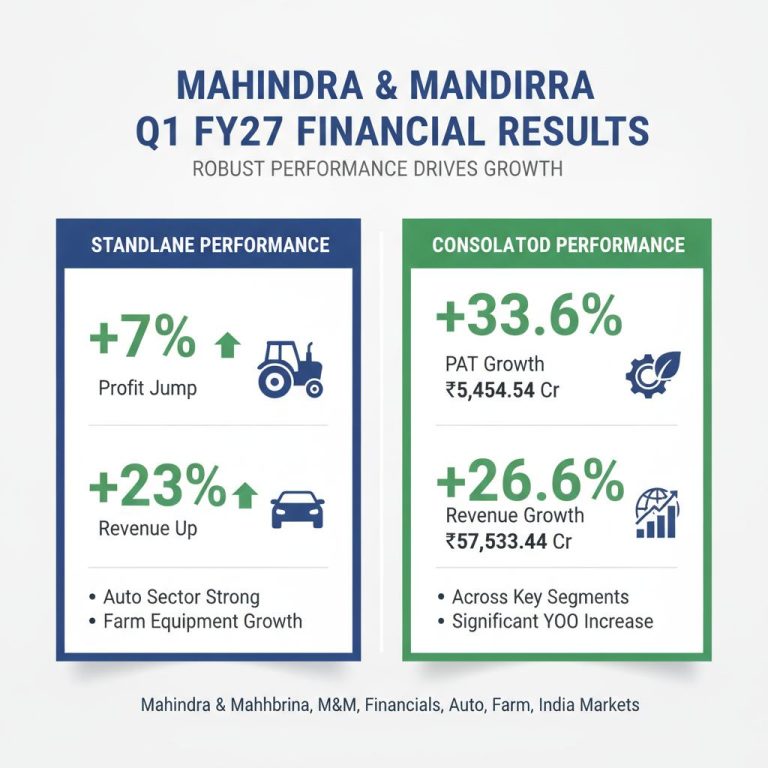

Hands use a magnifying glass to review IRS 1099-R forms on a wooden table.

For many working Americans, the 401(k) plan is a cornerstone of retirement savings. It offers a convenient way to contribute pre-tax income, often with the added benefit of an employer match – essentially free money. However, a significant financial risk often gets overlooked: the impact of Required Minimum Distributions (RMDs).

Once individuals reach a certain age (73 or 75, depending on their birth year), they are mandated to withdraw a specific amount from their 401(k) accounts annually. Failure to do so can result in substantial penalties. These RMDs are not merely an administrative detail; they can have serious financial consequences.

The primary concern is that RMDs can unexpectedly push retirees into higher tax brackets. This means a larger portion of their retirement income will be taxed. Furthermore, increased retirement income due to RMDs can lead to a greater portion of Social Security benefits being subject to taxation. Additionally, higher income levels in retirement can trigger surcharges on Medicare premiums, adding another layer of cost.

The size of the RMD is directly tied to the 401(k) balance. As balances grow over decades of consistent contributions and market growth, RMDs can become substantial. If a retiree does not need all of this mandatory withdrawal for living expenses, it can create a complex tax situation.

Fortunately, there are strategies to mitigate the impact of RMDs. One effective method is to perform Roth conversions before RMDs begin. By converting funds from a traditional 401(k) to a Roth IRA, those assets become tax-free in retirement and are not subject to RMDs. This strategy allows for tax-free growth and withdrawals later on.

Another approach involves strategically managing 401(k) withdrawals in the years leading up to RMD age. Taking larger distributions during periods of lower income, such as the time between leaving full-time employment and starting to collect Social Security, can help reduce the overall tax burden later. This proactive withdrawal strategy can lower the 401(k) balance at the point RMDs commence.

While 401(k)s are invaluable tools for accumulating retirement wealth, understanding the potential drawbacks, particularly RMDs, is crucial. By planning ahead and employing strategies like Roth conversions or strategic withdrawals, individuals can better manage their tax liabilities and ensure a more secure financial future in retirement.