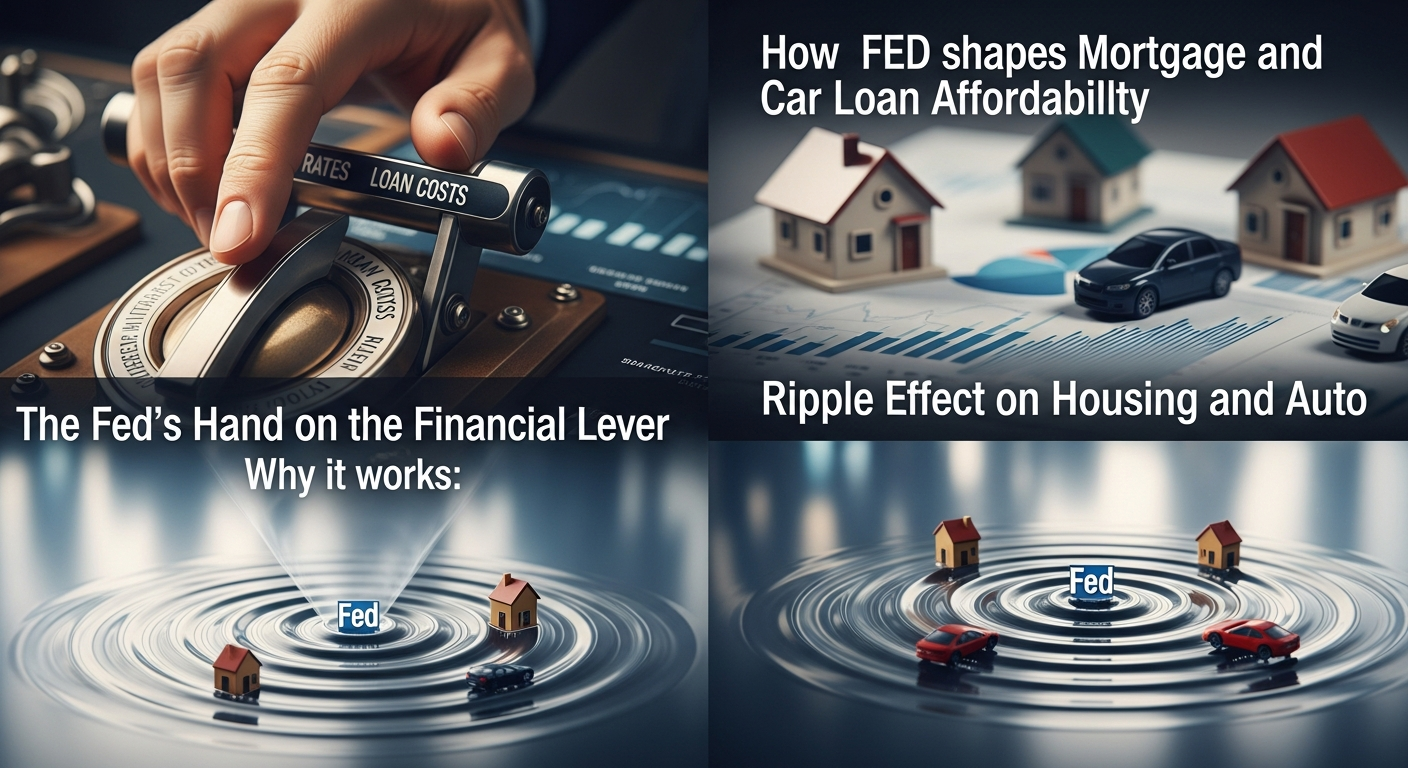

In the realm of personal finance, the Federal Reserve (the Fed) holds significant sway, particularly when it comes to the affordability of major purchases. From mortgages to car loans, the Fed’s decisions on interest rates directly influence how much Americans pay for these essential components of the American Dream.

Context: The Fed’s Role in Affordability

The Federal Reserve’s primary tool for influencing the economy is the federal funds rate, the target rate that banks charge each other for the overnight lending of reserves. When the Fed raises this rate, it becomes more expensive for banks to borrow money, which in turn increases the interest rates they charge consumers for loans. This includes mortgages, car loans, and even credit card debt. Conversely, when the Fed lowers rates, borrowing becomes cheaper, potentially boosting demand and economic activity.

Analysis: Mortgages and the Housing Market

Mortgages are perhaps the most visible example of the Fed’s impact. As interest rates rise, so do mortgage rates, making it more expensive to buy a home. This can lead to decreased demand in the housing market, potentially slowing down price appreciation or even causing prices to fall. Conversely, when the Fed lowers rates, mortgage rates often follow suit, making homeownership more affordable and potentially stimulating the housing market. The interplay between the Federal Reserve and the housing market is a crucial aspect of understanding the broader economy.

Analysis: Car Loans and Consumer Spending

The effects of the Fed’s decisions extend beyond the housing market. Car loans, another significant expense for many households, are also directly affected by interest rate changes. Higher interest rates make car loans more expensive, potentially leading consumers to delay purchases or opt for less expensive vehicles. This can have a ripple effect on the auto industry and overall consumer spending. Conversely, lower rates can make car purchases more attractive, potentially boosting sales and contributing to economic growth.

Implications: Economic Policy and Household Budgets

The Federal Reserve’s monetary policy decisions are a balancing act. The Fed must consider inflation, employment, and economic growth when deciding whether to raise or lower interest rates. These decisions have far-reaching implications, not only for the financial markets but also for the daily lives of American consumers. Understanding how the Fed’s actions affect mortgages, car loans, and overall affordability is essential for individuals and businesses alike.

In conclusion, the Federal Reserve’s influence on the affordability of mortgages and car loans is undeniable. As the Fed navigates the complexities of economic policy, its decisions will continue to shape the financial landscape for individuals and businesses across America.