Suze Orman presenting on Social Security at a studio.

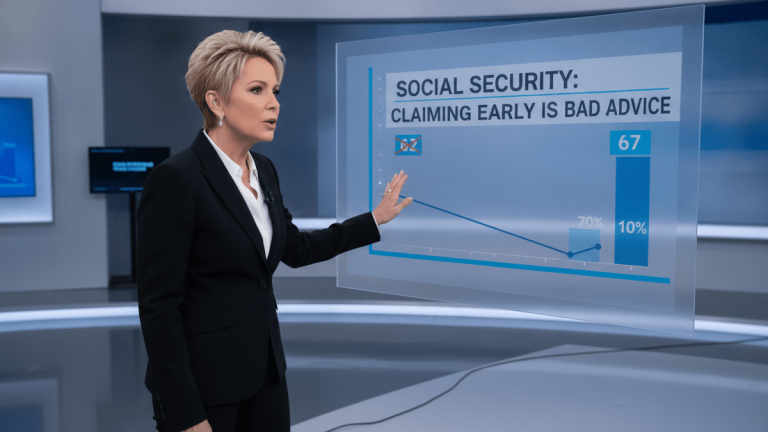

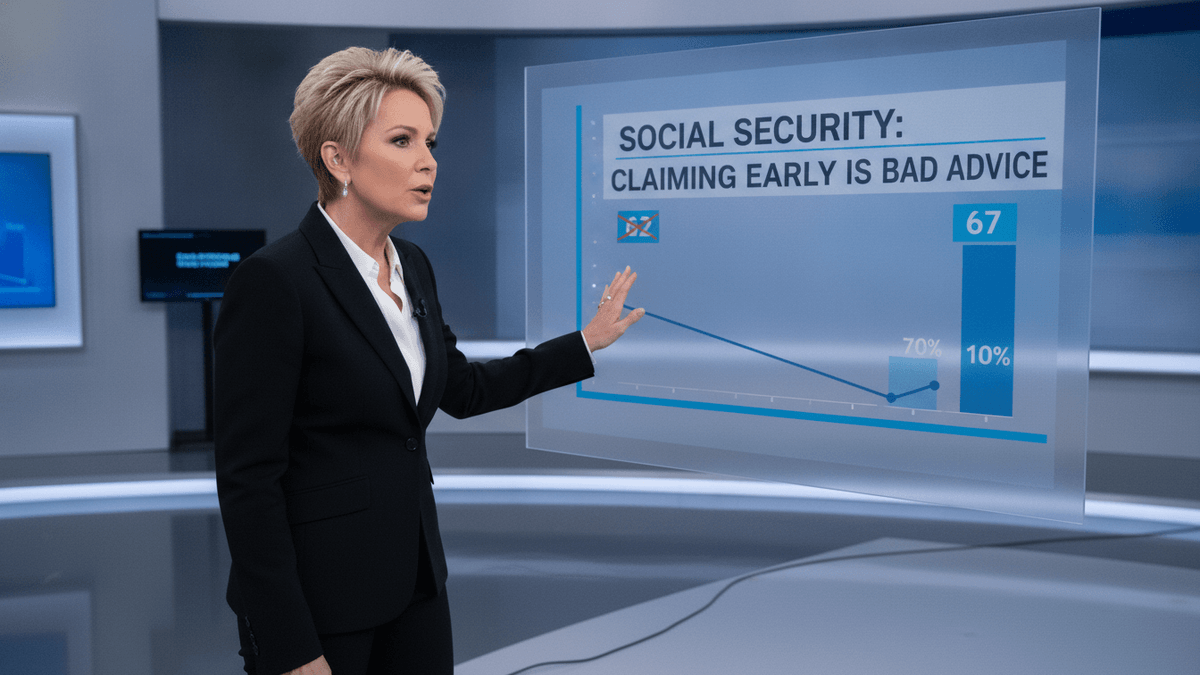

Financial expert Suze Orman is sounding the alarm against a growing trend of Americans claiming Social Security benefits early, particularly at age 62, due to fears about the program’s long-term solvency. Orman asserts that this widely circulated advice is detrimental, as it locks retirees into a permanent reduction in their monthly payments.

The Social Security Administration’s 2026 Trustees Report indicates that the program’s main trust fund is projected to be depleted by the fourth quarter of 2032. Following this depletion, ongoing tax revenues are expected to cover only 78% of scheduled retirement benefits. Despite this, Orman argues that claiming early is a misstep that can have irreversible financial consequences.

“For anyone born in 1960 or later, your Full Retirement Age is 67. That is when you are entitled to 100% of your earned Social Security benefit. If you choose to start collecting at 62, you receive just 70% of that benefit — a 30% reduction that is locked in permanently,” Orman explained on her website. She emphasized that this early claim essentially amounts to accepting a significant, unchangeable penalty.

Orman also addressed concerns that claiming early secures benefits before potential cuts. She noted that even in a worst-case scenario where Congress takes no action, Social Security would still be able to pay out approximately 80% of scheduled benefits, a 20% reduction. She referenced historical instances, such as the early 1980s, where solutions were found to address funding challenges without beneficiaries bearing the full cost.

To illustrate the impact, Orman provided an example: a $2,000 benefit at age 67 would be reduced to $1,400 if claimed at 62. If a 20% cut were applied in the future, the individual who waited until 67 might see their benefit drop to $1,600, while the early claimant would receive around $1,260.

Orman identified two exceptions for claiming Social Security early: significant health issues or an inability to work or access retirement savings. However, she strongly advocates for waiting until age 70 to claim benefits, as this maximizes the monthly payout. For married couples, she specifically advises the higher earner to wait as long as possible, ideally until age 70, to ensure the surviving spouse receives the larger benefit, calling it a crucial financial gift.